https://econsultancy.com/ashley-friedlein-marketing-digital-trends-decade-2020-to-2030/

This is a special year. 2020 always used to be ‘the future’ somewhere on the horizon. Well, here we are. We need a new future. Let’s go with 2030.

There have been quite a few ten-year retrospectives written on digital, and some (fewer than usual for some reason) 2020 trends and predictions, but not much looking forwards ten years. So that is what I would like to focus on first.

You can use the quick links below to navigate. And we’ve also created a downloadable PDF, which you can get for free here.

The decade to 2030:

- 1. In search of trust

- 2. Humane tech

- 3. Personalisation 2.0

- 4. Everything-as-a-service

- 5. Ecommerce and the environment

2020 Digital and marketing trends:

- 6. Ecommerce, social, advertising, UX, SEO etc.

- 7. Messaging

- 8. Digital & marketing transformation

- 9. Data

- 10. Customer Experience

The decade to 2030

What will digital/marketing look like a decade from now in 2030?

We know, of course, that there will continue to be advancements in technology, both hardware and software, and artificial intelligence is likely to bring about the greatest changes.

Quantum computing could also deliver seismic change within the next 10 years. Last September Google claimed ‘quantum supremacy’ in performing a calculation that would have taken a traditional computer around 10,000 years to complete in a mere three minutes and 20 seconds.

But here are five broad trends I see playing out in the coming decade.

1. In search of trust

Research has confirmed what we already expected: there has been a loss of trust.

People are shifting their trust to relationships within their control. Trust in institutions, companies, politicians, even brands, has been eroded. Trust in ‘big tech’ companies is also fragile in the wake of data and privacy scandals. Fake news has further undermined our trust in supposed facts.

Recent research from YouGov and Grey London into the levels of consumer trust in influencers and social media in the UK revealed that 41% of regular social media users say they have seen inaccurate content over the last month and 48% believe that profiles of celebrities are either ‘not at all honest’ or ‘somewhat dishonest’.

And yet Edelman’s 2019 Trust Barometer research found that 81% of consumers agree that trust is a deal breaker or deciding factor in their buying decisions. Perhaps understandably, trust is becoming more important as it becomes scarcer.

For marketers, and brands, this is critical and the battle of the next decade will be about (re)gaining trust with customers. Coming up with a new ‘purpose’, touting your ‘values’, claiming ‘authenticity’ and ‘transparency’ alone won’t cut it.

So how can we deliver trust in the coming ten years? Three areas stand out for me.

Consistency

There are various areas of branding that don’t get enough attention (salience, distinctiveness…) but consistency is certainly one. Professor Mark Ritson has written about the importance of brand ‘codes’, built consistently over time.

You might not like Trump, nor describe him as ‘trustworthy’, but you can perhaps trust what to expect from him? Even his inconsistency is consistent. ‘Get Brexit done’ was successfully consistent.

In our attention-addled world it takes time and persistent consistency to get through and create the potential for trust.

Playing with brand codes: Cadbury removed wordage from its packaging to support Age UK, donating 30p to the charity for each one sold.

We’re thrilled to be working with @CadburyUK on #DonateYourWords, a campaign to help tackle #loneliness.

Cadbury has donated the words from their Dairy Milk bars and will donate 30p from every sale to @age_uk to help us provide vital services & support: https://t.co/qfgI4BMryw pic.twitter.com/2PZv9DpZd1

— Age UK (@age_uk) September 4, 2019

https://platform.twitter.com/widgets.js

Experience

There is a reason ‘customer experience’ has been, and remains, such a hot trend in digital and marketing. Trust can’t be claimed, it has to be earned. And the most important proof point in deciding whether to trust a brand is not how good its advertising is but what your (or others’ you trust’s) experience of the brand is.

You have to deliver on experience to build a trusted brand: “A good brand is a promise, a great brand is a promise kept” Tom Sitati, Director, Brandscape.

Humanity

Machines are already better than humans in many areas including, for example, image and speech recognition. This past year we have seen demos of machines holding conversations that are indistinguishable from actual humans. Computers are creating new faces that we cannot tell are not ‘real’. James Dean is being brought back to life to star in a new film.

But do we trust these superhuman machines? The best drum machines play slightly out of time to mimic more ‘natural’ sounding humans. Humans might be spooked or threatened by machine perfection and be more trusting of brands which can show vulnerability and imperfection.

To build trusted brands, then, we must be careful not to rely too much on machines, data and automation, but seek to (re)connect on a more human level.

Read more on this topic in the 2018 Econsultancy report Trust, Transparency and Brand Safety.

2. Humane tech

Related to the last point, we have also seen the emergence of “humane tech”, “calm tech” and other initiatives to try and redress the sense that technology is currently designed to manipulate our behaviour and exploit our psychological vulnerabilities.

Sacha Baron-Cohen’s November 2019 speech at the Anti-Defamation League confronted this head on and books like Nir Eyal’s “Hooked” have revealed how it is possible to design for addiction.

In DigitalAgenda’s green paper Power & Responsibility: 10 challenges and 10 ideas for change in the digital age the authors chart an evolution from tech euphoria, to tech fear (where we are now), to humane tech.

Philosopher Alain de Botton has challenged society to ask what has happened to ideas like ‘consolation’, ‘meaning’, ‘kindness’, ‘wisdom’.

The mantra of the last decade was “move fast and break things”. Perhaps now we need to work together and fix things? “Do now, think later” might concede ground to consideration, thought and respect? Fast is now faced with slow food, slow fashion, slow travel.

As the world has become increasingly connected, it has also become noisier. We struggle to focus on the things that matter. “Technology shouldn’t require all of our attention, just some of it, and only when necessary” says Amber Case in her book on designing calm technology.

There is evidence of a backlash against overly invasive and addictive technology. Mediacom’s 2019 ‘Connected Kids’ report found that Gen Z are taking steps to reduce their digital usage: 18% of 8–19-year-olds in the UK have deleted social media apps in response to the apps’ negative effects and 13% said they have cut down their social media usage, with 17% also limiting their screen time.

As brands, and marketers, over the next ten years what are we then to do?

Very few of us are big enough just to try and shout louder than the rest. Instead we really do have to understand our brand essence, more than ever before, and find ways to make that connect with our prospects and customers in a more human way.

We will need to make conscious decisions about what we stand for as brands and businesses and the implications for how we therefore use technology. We understand why streaks in Snapchat, duets in TikTok, or video auto play in YouTube or Netflix, work to drive usage but are these appropriate ‘tricks’ for our brands?

TikTok: Everything you need to know

Of course, over the next ten years we will have ever more ‘human’ data sources available including biometric and sensory ones: voice, language, touch, sentiment, expression, mood etc. Recently Facebook bought a ‘brain-machine-interface’ start up called CTRL-Labs that is working on ways for people to control devices simply using brainpower.

But for most of us I believe the opportunity in the next ten years isn’t actually about futuristic technological capabilities. We aren’t using most of the technology already at our disposal. The real opportunity for most marketers is still to create brands, propositions and ideas that tap into the emotional, irrational, messy and imperfect world of real humans – albeit often using technology as an enabler.

3. Personalisation 2.0

Where does all this talk of trust and humanity leave perennial trend-darling ‘personalisation’ then?

According to our recent research with Adobe for the 2020 Digital Trends concern around how customers felt about their data and privacy ranked in the top three most significant business worries.

Then there was GDPR. And now CCPA in California. In 2019 Firefox and Safari started blocking third-party cookies by default and Chrome introduced anti-tracking measures. Apple continues to make changes to Intelligent Tracking Prevention (ITP) in Safari, making (re)targeting and measurement of iOS audiences a challenge.

Talk about taking back control. It looks like the sovereignty of self is also a movement.

How are we meant to personalise if we have no personal data?!

It gets worse. Gartner recently predicted that 80% of marketers will abandon personalisation efforts by 2025 due to “lack of ROI, the perils of customer data management or both”.

However, I don’t think personalisation is going away but it does need redefining. Actually, it has never been very well understood anyway – what is targeting vs customisation vs personalisation? If we’re honest, actual individual-level ‘personalisation’ for most has only extended as far as “Hi [first name]” in emails anyway.

The challenge, and opportunity, of “Personalisation 2.0” is about delivering the personalisation customers actually want whilst respecting the privacy they expect.

Oxymoronic as it sounds, this means we need to get good at “anonymous personalisation”.

Great waiting staff, great landlords/landladies, or the famous village shopkeeper don’t actually need to know who you are to give you personal attention and cater to your needs. The sales assistant who can see you looking lost in a shop, offers to help and walks you to the product you seek whilst informally chatting doesn’t need to know who you are to deliver an experience that feels very personal.

Digital experiences too can feel personalised without actually having to know who you are. I could pass you my phone and you could use Uber and it would feel personalised to you – you choose the car, you get it to come to you, you can see it coming live, you get the updates, you leave the feedback (yes, ok, I pay…). Maybe it is coming soon but even Uber doesn’t use the data it has about me to try and do clever ‘personalisation’ like predictive journey suggestions. And I might not want it.

As customers we want to be recognised without necessarily being identified; we want to be treated as if each business cares; we want customisation according to the context and circumstances; we want ease and convenience; we want less friction; we want to be able to express our needs without judgement.

All these things engender a feeling of ‘personalisation’ but can be done without personally identifiable information.

Personalisation 2.0, therefore, will focus on:

- Simple, intuitive, friction-free, ‘effortless’ user experiences.

- Capturing explicit preferences from customers (“zero party data”) that do not necessarily require them to be personally identifiable.

- Using available non-personal data signals, enhanced by the predictive power of machine learning, to near-magically adapt to the particular context and environment to super-serve customers’ needs and goals in the moment.

- Maximising intimacy and relevance without infringing privacy.

- Allowing users to configure and control their experiences in realtime without having to give up their personal privacy.

- Building zero/first-party relationships based on transparency and trust but which don’t necessarily involve revealing actual identities.

4. Everything-as-a-service

We know about the rise of the gig economy and the subscription economy. Royal Mail forecasts that the value of the subscription market will have increased 72% over the five years to 2022.

There is pretty much nothing we don’t now subscribe to: content (Netflix etc.), food (Hello Fresh etc.), shaving (Cornerstone etc.), office space (WeWork etc.), sex toys (Teaserbox etc.).

We know also about the rise of software-as-a-service (SaaS) as part of the wider move to the cloud. There is also PaaS (platform-as-a-service) and IaaS (infrastructure-as-a-service). Further on in this article we’ll consider DaaS (data-as-a-service).

Over five years ago I suggested it was time for marketing-as-a-service and three years ago encouraged us all to think of your product or service from a subscription mindset.

Over the next ten years we should consider “everything-as-a-service” as we build business models, products, propositions and brands.

We need to be (re)configurable, scalable, modular. We need network and ecosystem thinking. Being available on demand and adaptive to the context in which we surface will be a pre-requisite for success.

This applies not just to data, systems and applications but to processes, people and organisational structures. Agile is just the beginning.

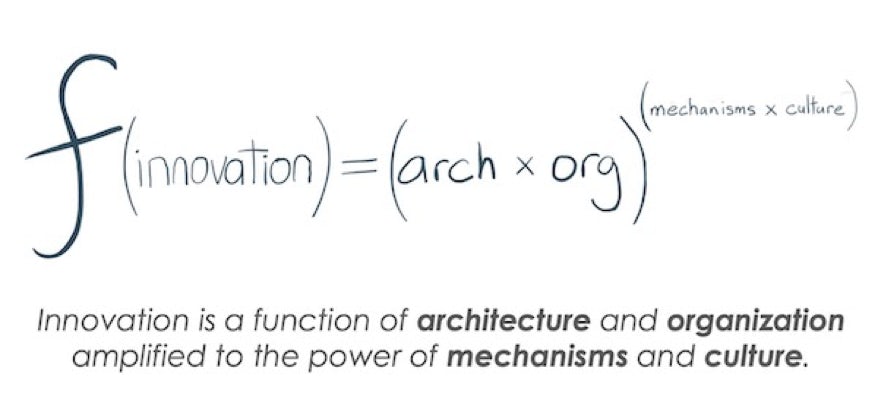

This way of thinking goes back a long way. In the classic, and hilarious, Stevey’s Google Platforms Rant he explains Amazon’s Jeff Bezos’s ‘Big Mandate’ of 2002, that all teams would henceforth expose their data and functionality through service interfaces and these interfaces must be designed from the ground up to be externalizable (to be exposed to developers in the outside world).

Jeff had the vision of EaaS almost two decades ago. Scott Brinker featured some great insight into Amazon’s innovation formula last quarter, based on a talk at the MIT Platform Strategy Summit by Dirk Didascalou, VP of IoT at Amazon Web Services (AWS), and captured in this graphic which Scott created:

We examine and explain the elements of this formula in our Digital Shift Report: Q4 2019 but you can see that the original technology-as-a-service vision has extended into the organisation to include how it is structured, how work gets done, and even the culture.

The next ten years will see us not just trying to break down data and technology into more reusable and composable parts, but service-oriented thinking will also continue to change how we structure our organisations and how we get work done.

From a marketing point of view, we have already mentioned the codes that should underpin brands – elements that can be re-composed to great effect. We are seeing design move beyond designers towards design systems that embrace atomic design and other patterns to deliver what we might call ‘design-as-a-service’. If we can crack our brand and design codes and build a system to bring them to life then, perhaps, we will have discovered the DNA of customer and brand experience.

This coming decade requires us to break down everything into micro services and figure out how to orchestrate the assembly, and constant re-assembly, of the component parts to deliver amazing experiences for our prospects, customers, staff, and other stakeholders.

5. Ecommerce and the environment

We have been under the impression that ecommerce is positive for the environment as it means fewer shopping trips requiring a journey by car.

However, there is increasing evidence, particularly as our shopping behaviours themselves change, that ecommerce might actually be the least environmentally friendly way for us to shop. If so, as the pressures to tackle climate change through more environmentally-friendly ways of living increases in the coming decade, it is only right that ecommerce comes under much greater scrutiny and we may have to rethink, or at least adjust, its operating model.

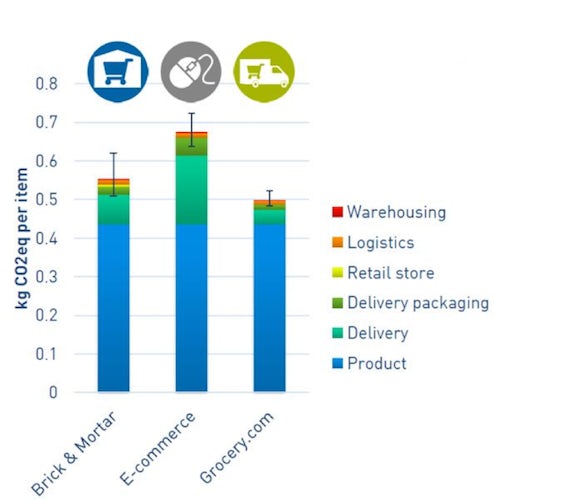

Unilever is known for its commitment to reducing the environmental impact of what it does. The consumer goods giant worked with industry body SEAC (Safety and Environmental Assurance Centre) examining its own data and industry analysis of the supply chain to work out the CO2eq emissions per item for different routes to market, including ecommerce and store sales, for various beauty and personal care products.

The results vary by country and product but the chart below, showing the UK data, identifies ecommerce as a worse offender than store sales, largely because of the extra emissions caused by packaging and delivery.

We all recognise the cardboard packaging of home deliveries. An artefact which lasts just minutes as we open our delivery and put the packaging straight in the recycling. Amazon is making efforts to reduce its packaging and last August announced it would fine other vendors on its platform who over-packaged their products.

But Amazon’s carbon footprint is still not far off that of Denmark or Switzerland and 30% of the solid rubbish the US generates now comes from the packaging of home-delivered products. Around a billion trees need to be cut down just to provide the ecommerce packaging for the US and the packaging for Christmas returns alone emits an additional 15 million tons of carbon into the atmosphere.

Since 2000 there has been a rise of 9% in passenger car miles on Britain’s roads. However, there has been a 56% rise in the number of miles travelled by home delivery vans in the same period. It seems ecommerce is making traffic worse not better.

The inconvenient truth we need to face in the coming decade is that it is the very same ‘effortless customer experience’ that we strive to deliver that is also driving an ecommerce revolution that may be damaging the planet we’re trying to protect.

There was a time when you waited days for an ecommerce delivery. That window has shrunk to specific same-day slots. With internet of things, delivery to car boots or home access, fridges auto-replenishing and so on… the end game of the ideal home delivery experience is that we forget that anything is being delivered at all. Shipping will become incidental to the purchase experience.

For a long time, we have been part of the supply chain getting goods the ‘last mile’ to our homes. But soon why even walk ten minutes to a shop when it can painlessly and near instantaneously come to you?

Thankfully, whilst ‘digital’ might be more part of the problem than we have recognised, it can also be part of the solution. OLIO, for example, uses technology to connect neighbours to share food, and other things, rather than throw them away. Reusable packaging solutions like LimeLoop and RePack are emerging. Technology is helping power the ‘circular economy’ which encourages reuse, recycling and a reduction in waste.

2020 Digital and marketing trends

So much for the ten-year perspective megatrends. What can we expect in 2020?

6. Ecommerce, social, advertising, UX, SEO etc.

To get the low down on what we can expect across a range of specific digital marketing disciplines I recommend you check out the 2020 trends and predictions we’ve collected from our trusted industry experts:

- Ecommerce trends in 2020

- Social media trends in 2020

- Digital advertising trends in 2020

- CX and UX trends in 2020

- SEO trends in 2020

And the following are excellent short briefings on specific platforms and media that offer new opportunities for marketers over 2020:

- Getting started with TikTok: A guide for marketers

- Getting started with Instagram: A guide for marketers

- Programmatic TV advertising

- Future trends in customer data platforms

- The new age of audio: What does it mean for advertising?

7. Messaging

In my 2019 trends I opened with the observation that there were “no new digital marketing disciplines”. That remains broadly true for 2020.

However, messaging is interesting as, like email and social media before it, it is an entirely new medium. At least relatively ‘new’ from a marketing and business perspective. And a medium that is growing very fast.

In 2019 there was a lot of hype around ‘conversational marketing / UI’ that centred mostly around chatbots. That has largely fizzled out. But the level of conversations taking place in messaging apps – both in addition to, and instead of, other forms of communication like email – continues to rise sharply.

It seems certain that we as marketers will need to understand and embrace this new medium in the same way as we had to grapple with email and social before. It is likely we will follow the same adoption trajectory: at first there will be specialist roles and technologies; then there will be confusion and tension over who ‘owns’ messaging as a medium; then we will seek to integrate messaging across the organisation as just another touchpoint in our omnichannel world.

As a medium, messaging has many different applications and opportunities for digital and marketing practitioners. Including the following:

7.1 Advertising in messaging apps

Snapchat recently reported that total users are over 210 million globally (up 24 million users year-on-year) and a revenue increase of 50% year-on-year to $446 million in Q3 2019. In the US they have just introduced a new “Dynamic Advertising” option which allows brands to sync a product catalog and select specific audience and campaign objectives for Snapchat to then deliver ads in real-time, adjusting product changes like price or availability to match stock levels.

Instagram meanwhile launched its highly anticipated camera-first messaging app, Threads, allowing users to share their Stories, private messages, videos and more with their Instagram close friends. Instagram is also launching “Reels” which many see as Facebook’s answer to TikTok as it focuses on short from (15 sec) video content. The Top Reels section on Instagram’s Explore page gives the most popular Reels the opportunity to go viral on the platform.

Last year Facebook also announced that adverts will be coming to WhatsApp in 2020 and the back ends of Instagram, Messenger and WhatsApp are being integrated to allow data and messaging to travel much more freely between them.

There are plenty of opportunities, therefore, for marketers to get creative with innovative new advertising formats and achieve real reach. As well as paid media there is the opportunity to engage consumers in the feed or via stories if done well.

The brave may even consider how to run their own customer groups and communities on messaging apps. For example, Tango Squads, Adidas’s community initiative to engage young footballers, has used Messenger and WhatsApp.

7.2 Payments & ecommerce via messaging

Facebook Pay is now available in the US. Users can make seamless product purchases on any of Facebook’s three messaging apps: Instagram, WhatsApp and Messenger. Currently payments are restricted to transfers, person-to-person payments, and payments to businesses on Facebook Marketplace.

In certain countries, WhatsApp for Business now allows SME business customers to provide a mobile storefront for customers to browse and discover their products. Couple this with seamless payment options, as above, and suddenly the gap between messaging and commerce disappears.

Social commerce has not yet taken off in the West quite as much as it has in Asia. And ‘messaging commerce’ is an even newer subset of this. But 2020 will see more brands, marketers and ecommerce practitioners experimenting with this huge opportunity.

7.3 Professional & business messaging

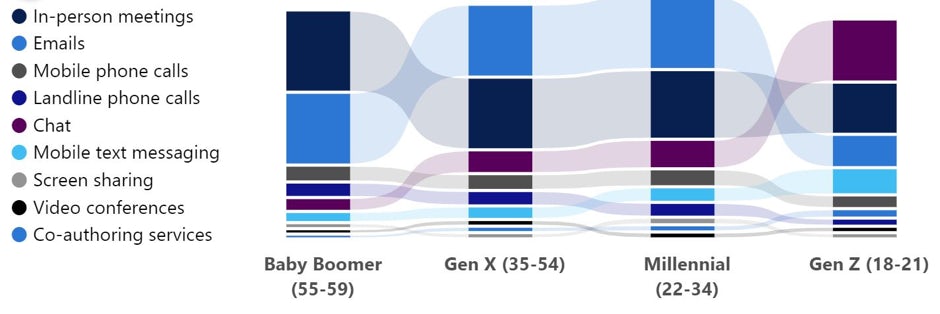

This is an area I am particularly close to as, whilst not busy with Econsultancy, I also run Guild, a premium messaging app for professionals and businesses. Econsultancy runs various groups on Guild for our subscribers as well as our CMO ‘Digital Advisory Board’.

Even in 2018 a Microsoft study of 14,000 professionals showed a stark difference across the generations with Gen Z almost as happy using chat apps to speak to colleagues as they are setting up face-to-face meetings. The chart below from the research shows the different communications methods used at work across the generations. Chat is shown in purple and clearly increases significantly, at the expense of email, phone and in-person meetings, in the younger generations.

From a marketer’s point of view, it is even more interesting to see how fast messaging is growing as a medium for stakeholders external to the organisation, including prospects and customers. Facebook’s research into consumers’ behaviour and expectations around messaging businesses, Why Messaging Businesses is the New Normal, showed that the majority of those surveyed had messaged a business in the previous quarter. Those surveyed in emerging markets were 2.4x more likely than those in mature mobile markets to say they message businesses. The benefits customers cited were: easy to use, anywhere, any-time, time-saving, effective, reliable, documented, fun, real time/fast.

According to the research “…the majority say being able to message a business helps them feel more confident about the brand. By helping to establish confidence and trust, messaging can uniquely draw people and businesses together into an ongoing conversation, ultimately enabling more meaningful connections than ever.”

There are obvious applications for messaging apps around customer service, like KLM’s use of WhatsApp, but 2020 will see messaging become a greater part of businesses’ communications infrastructure and marketing both internally and externally with customers, suppliers and other stakeholders.

8. Digital & marketing transformation

Last year I wrote about digital transformation and the year before about a new operating model for marketing. We may have moved beyond infancy in digital transformation but we are very far from adult.

We are entering turbulent years as transformation teenagers seeking to understand what exactly it means for us as things continue to change.

8.1 Culture

We have learned that digital transformation is not just about technology and data. It is also about business models, leadership, people, process, mindset and culture.

2020 will continue to see us wrestle with new ways of working, new ways of organising ourselves and embedding news skills, capabilities and mindsets. The table below, taken from Econsultancy’s “Effective Leadership in the Digital Age” summarises the differences between more traditional business cultures and ‘digital’ ones.

8.2 People, roles and capabilities

‘Digital’ is proving remarkably resilient in job titles. Just when it looked like we had passed ‘peak CDO’, Unilever recently announced it is creating a chief digital and marketing officer role to ensure the business is ‘future-fit’.

Variants of CMO / Marketing Director continue to flourish with the words ‘customer’, ‘digital’, ‘experience’ and ‘growth’ often seen. Personally, I think it is better to try and clarify, even redefine, what a CMO does, and what marketing is, than come up with new job titles.

The impetus behind our Modern Marketing Model (M3) was to provide a framework for marketing that embraced both ‘classic’ marketing and digital marketing so we did not need such existential job title angst. But, as Russell Parsons, editor of Marketing Week acknowledges, for 2020 we can expect more of the same.

One area where more consensus has been achieved is the recognition that marketing needs to balance both the long and short term to be effective. Mark Ritson wrote about Binet and Field’s famed research last year and also refers to ‘two-speed’ branding which consciously allows for both a short-term focus, typically more sales-activation and conversion oriented, whilst investing in longer-term brand building to build a platform to reap future rewards. In 2020 we can hope to see more ‘long term digital’ thinking and increased efforts to marry digital and classic marketing as part of this move to deliver in the short term and the long term.

An area where there is much less clarity, and therefore some confusion and tension, is between ‘Marketing’ and ‘Product’. The importance of ‘product’ as a function, and the roles within it, has risen in recent years. In part, this is because of all the new start-ups and scale-ups championing the role of product manager as learned from Silicon Valley. In part, it is also due to the rise in importance of technology-enabled customer experience. ‘Product’ typically sits at the intersection of technology, the business, and the customer.

Product management can be part of the remit of a modern marketing function given its customer focus. The problems is, like ‘digital’ and ‘data’, many marketers just don’t understand this new discipline well enough to manage it and integrate it properly with everything else they are doing. 2020 will thus see more friction but hopefully, with experience and training, greater cooperation and reconciliation between ‘marketing’ and ‘product’.

8.3 Process

‘Marketing ops’ is a few years old now. Just as marketing is learning agile from the world of software development, we are creating marketing ops in a similar vein to the dev ops technology function.

The main job of marketing ops is to help wire up all the data, and align various mappings, migrations, processes and data/logic flows, within a governance framework, so that all the marvellous omnichannel real time personalisation experiences we talk about are even remotely possible to deliver.

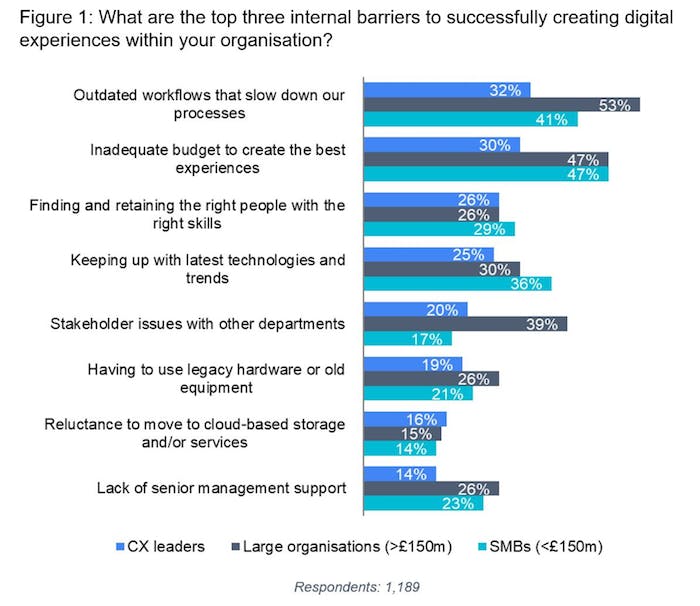

However, one of the interesting findings from Econsultancy’s research with Adobe to produce our joint 2020 Digital Trends report, is that “outdated workflows” are the number one problem for organisations trying to deliver better customer experiences – see the chart below. For 2020, then, we can expect a lot of the work on improving processes to be around how to optimise workflows and prevent them from being the barrier they currently are.

Digital Transformation: 2019 in Review

9. Data

We have been told that data is the new oil. We do not have a problem finding and extracting this data oil. We have a glut of data crude oil. But we do have a problem refining it and turning it into something disproportionately valuable. 2020 will see us working on the following as the new frontiers of data.

9.1 Data digitalisation

Econsultancy’s recent Digital Transformation and the Role of Data report makes the case for the need for a data transformation to take place before digital transformation is fully possible.

The table below, taken from the report, does a great job of showing how we need to move beyond the ‘crude oil’ state of data where we merely digitise it to a much more refined state of digitalisation where we use data to create and liberate new value.

9.2 Data-as-a-service (DaaS)

Also elaborated in Econsultancy’s Digital Transformation and the Role of Data is the idea of “data-as-a-service” (DaaS). This is a powerful idea and makes possible a lot of the other trends discussed in this article including atomic design, personalisation 2.0, and ‘everything-as-a-service’. DaaS enables the creation of modular systems that enable, for example, personalisation at scale without complete chaos.

The report’s author, Laura Chaibi, describes DaaS as follows: “Data can also become a service underpinning business, built on the premise that data serves multiple clients and stakeholders with varying needs to be met at the same time.

“Data-as-a-Service (DaaS) is a data framework that essentially splits data access and usage from where the data is stored, freeing the data for multiple uses with speed and ease of access and the ability to scale usage. DaaS data agility is a substructure of digital transformation acting as a reinforcement to solutions enabled through digital transformation. DaaS data can permeate all corners of businesses and how they run with the aim to amplify capabilities and sustainably scale.”

From a marketing perspective this means that DaaS enables:

- A centralised holistic view of consumers and customers and their relationship to the business, products and services and across an industry.

- Tracking the touchpoints consumers and customers have across lines of business.

- Building out metadata for wider context about the touchpoints tracked, to create new solutions, products and services.

- Understanding customer history and building out a profile of customer preferences.

- Understanding and prioritising valuable customer segments and where to focus strategies around audience segments and types.

- Working towards predicting customer behaviour and actions and eventually aiming to influence the favourable behaviour or actions from the consumer through prescribed marketing, product and service prompts.

- Fostering loyalty and minimising customer churn.

9.3 Data-driven operating models

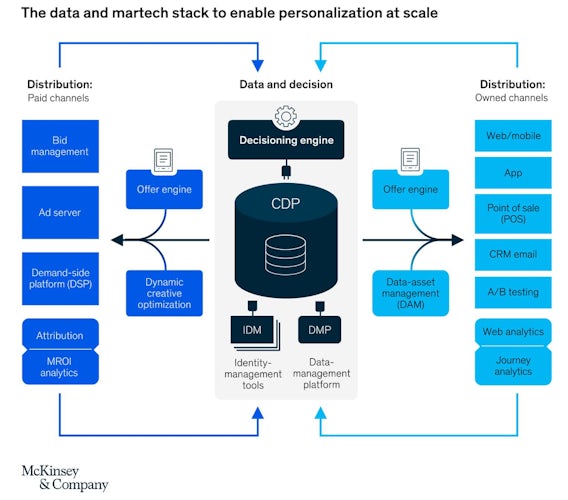

To date we have largely focused on data architectures, processes and workflows. This is understandable as it is a hard problem to tackle in its own right. For example, the diagram below, taken from McKinsey’s “A technology blueprint for personalization at scale”, shows a proposed architecture for resolving the complexities around CDPs, DMPs, DAMs, DSPs etc.

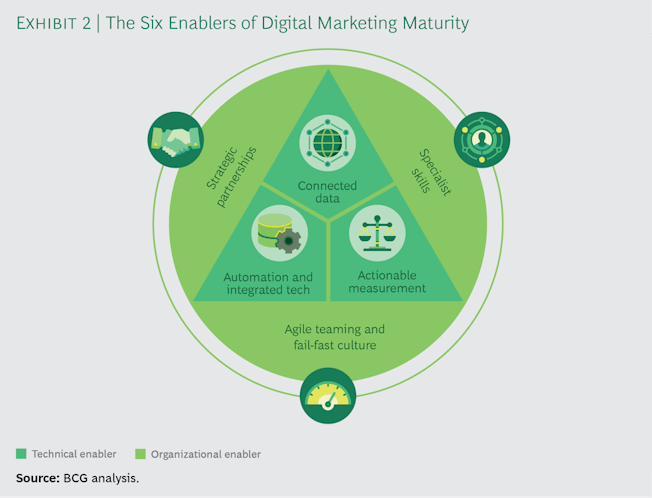

Once we have figured out the data ‘plumbing’ and got it flowing efficiently (made more powerful and adaptable by the aforementioned DaaS) then we are faced with creating an operating model for our organisations that can be data-driven. The diagram below, from BCG’s “The Dividends of Digital Marketing Maturity” suggests the key elements required to move towards this with ‘connected data’ just one of the six ingredients.

The picture becomes more complex when you consider that all this data is not just data within your direct control but exists outside your organisation too. 2020 will continue to see more (often open, increasingly realtime) APIs allowing data to be streamed between organisations and other entities.

In my 2019 digital trends I asked the question about the ‘brain’ needed to run this complex ecosystem. Many technology vendors offer decisioning engines that aspire to be this brain. But beyond specific technologies, this is more a question of figuring out the correct hypotheses, KPIs, rules or even AI to drive the system in an optimal way to deliver the desired business results.

In a fundamental way this a matter of strategy: you must encode your business strategy in your data and decisioning engines to reach the goal of a data-driven operating model. Over 2020 we will see ‘data’ continue to be an operational area of focus but it will also be the subject of more strategic initiatives.

9.4 Data in the dark

Whilst there is no shortage of data available, it is also the case that the richness and transparency of what we can see as marketers has been curtailed in the last years.

It began a decade ago when Google stopped providing the keyword data for searches that led to a visit to your site in Google Analytics. Since then we have had a combination of privacy regulation like GDPR, Apple and others preventing tracking via their browsers, and a behavioural shift into private communication spaces (in particular messaging apps) which are encrypted or provide very little visibility to marketers.

Over 2020 this has a number of implications:

- Ad spend will gravitate further to the big “walled garden” platforms but also to media owners who have a well-defined niche and first-party data.

- There will be renewed efforts by brands to get first party data rather than rely on second, or third, party data. Even more valuable than ‘observed’ first party data is customer-driven explicitly-expressed preference data – the aforementioned ‘zero party data’.

- Companies will look beyond current tracking methodologies to ‘post cookie’ alternatives, like device or behavioural ‘fingerprinting’, to try and establish unique identities. However, Google announced they will “aggressively restrict fingerprinting across the web” and there is no clear winner in the battle to offer a Universal ID

9.5 Data capabilities

The dearth of skills and capabilities around data is a well-worn challenge. Econsultancy research and best practice guides have repeatedly highlighted data as one of the key – usually lacking – skills of the modern marketer. This will continue to be a concern for 2020 and beyond.

10. Customer experience

We end on a trend that is very far from new but equally far from being over. Customer experience has consistently topped results of surveys into marketers’ key challenges and opportunities for years.

As with digital transformation, customer experience is no longer an infant but is entering its teenage years, trying to figure out exactly what it is and how it fits in. There are a few areas of CX, like voice, AR and VR, which have been hyped for a few years already but which will remain significant only for a few and experimental, if anything, for most over 2020.

10.1 Design is the new digital

If data has been the new digital for the last few years, then perhaps design is now taking over as the new digital. That exciting ‘new’ thing, with new job roles and ways of working, that no-one is quite sure how to fully embrace and where it fits in with business as usual.

“Design thinking”, as a user-centric way to address problems, has been around in earnest for several decades and began to emerge even earlier in the 1970s. But it is only now truly rising to greater prominence and brands like GSK are treating design as a strategic partner to marketing.

In part, this is because of the concomitant ascendancy of customer experience as a strategic imperative. In part, it is because all companies are becoming product/software companies to some degree. Certainly, the change in the world’s most valuable companies in the last decades points very clearly to organisations who espouse design thinking. More recently, the inside whispers among product scale-up businesses have let slip a secret new truth: you should have two designers for every engineer!

The value of design may now be recognised but, like with digital before it, there are new growing pains to deal with. As design teams grow there are questions and tensions around how it exists as a discrete function or not, what job titles and roles are right, what career progression exists, how the design capability is structured and it how it works with other functions.

“Design Ops” (like DevOps and Marketing Ops before it) is emerging as a specialist discipline to grapple with the growth and 2020 will see further such meta-roles as organisations create both specialist design roles whilst trying also to cajole broader multi-disciplinary teams into being more design-led.

Atomic Design, as per Brad Frost’s 2013 book of the same name, is not new but will continue to gain traction and attention over 2020. As we move towards design systems and processes, rather than isolated projects or deliverables, then the atomic design way of thinking makes a lot of sense. Its almost DNA-like approach to design fits very well with the trends towards ‘data/everything-as-a-service’, the increasing alignment of coding and design, and looking at data in a more modular and ‘componentised’ way.

In our search for efficiency and scalability, whilst maintaining the flexibility and adaptability to deliver different customer experiences across a whole range of screens, devices and touchpoints, the principles and methods of atomic design hold a lot of promise.

10.2 Customer need states

In 2020 we will continue to map customer journeys. And we will continue to try and remove pain points and friction. However, our efforts so far have largely been around documenting and improving existing operational tasks that we understand customers need to complete to interact with us. A lot of our efforts focused at first on digitisation and then, in recent years, we have endeavoured to deliver ‘omnichannel’ experiences.

This year it feels CX will begin to move beyond just transactional experiences and start to cater to customer need states and deliver to those also. It may be that those needs have nothing to do with digital or omnichannel. Primark has succeeded so far with no ecommerce and BT is returning to the High Street.

True, a common customer need is for experiences to feel effortless. Reducing customer effort should continue to be a core CX goal. Mobile, real-time, contextual, on demand, self-service, 24/7 availability… these will continue to be areas of focus for 2020. However, these things will become basic expectations before long.

Thinking harder about how CX can meet customer needs requires more nuanced insights, more innovation, around both practical and psychological needs. Ultimately, this might be around a customer’s mood, how they are feeling, how they perceive their relationship with you as a brand – including the themes of humanity and personalisation we addressed earlier. Equally, last year saw much discussion around brand values and purpose. CX has a vital role in bringing these to life.

Home delivery and packaging is one area of customer experience that is fast evolving to meet both brand needs (which might include reducing costs and environmental impact) and customer needs (which might include being able to take delivery when not at home as well as their own environmental concerns).

Drones have not yet arrived but the likes of Bloom & Wild’s “letterbox flowers” are delivered in boxes with different coloured interiors, depending on the collection and season, in boxes that fit perfectly through your letterbox. Home delivery wine retailers are experimenting with flat bottles made from recycled material which improves deliverability and reduces the environmental impact of using glass.

PillPack, owned by Amazon, is “a full-service pharmacy designed around your life”. They coordinate with your doctors and insurance to gather your prescriptions, schedule your first shipment and order your refills, package your medication by time of day and send them to you for free. If you don’t want to do this online you can even do it all by phone. This goes beyond modelling the typical customer journey across channels. It is a service that is very much modelled around the customer’s actual needs.

Ultimately the marketing opportunity is to take one’s brand, and what it stands for, and understand our customers’ need states, and marry those together in a way that works for both and feels like a natural, effortless, fit. The customer experience is the expression of that fit in action.

10.3 Workflow optimisation

As we saw earlier, according to our recent 2020 trends research with Adobe, “outdated workflows” are the number one problem for organisations trying to deliver better customer experiences.

For customer experience these workflows relate in particular to design and data, as we have already examined, but also content in the broad sense – any asset which needs to be created and managed as part of delivering an end customer experience.

Content, and content marketing, has mushroomed in recent years but we are now struggling to orchestrate and optimise that content in an efficient, co-ordinated and deliberate manner, particularly across channels and media. Roles and responsibilities around ‘content’ are still not always clear which compounds the workflow challenges. Over 2020, we will see the increased industrialisation, or ‘operationalisation’, of content and content marketing.

Tell us your thoughts – What do you agree with, disagree with, or think Ashley has missed? Let us know in the comments below.

Econsultancy can help

If your team needs upskilling in any of the areas discussed by Ashley, Econsultancy offers a variety of Fast Track training courses, as well as bespoke Marketing Academies. Subscribers can access all of our research, including Best Practice Guides, trends reports and briefings.

The post Ashley Friedlein’s marketing & digital trends for 2020 to 2030 appeared first on Econsultancy.

ramipril 5mg us order clobetasol online cheap astelin 10 ml for sale

purchase hytrin online cheap arava online sulfasalazine 500mg over the counter

generic isosorbide 40mg isosorbide cheap micardis usa

buy molnupiravir 200mg for sale cheap molnupiravir lansoprazole 30mg price

I do not know if it’s just me or if perhaps everybody

else encountering issues with your site. It appears like some of the text within your posts are running off the screen. Can somebody else please provide feedback

and let me know if this is happening to them too? This might be a issue with my web browser because I’ve had this happen previously.

Thank you